Across the UK, almost half a million people are living in a care home and for a large majority of those people, funding through their local authority is the best way to cover the cost.

In this article we’ll look at everything you need to know about local authority funding and residential care.

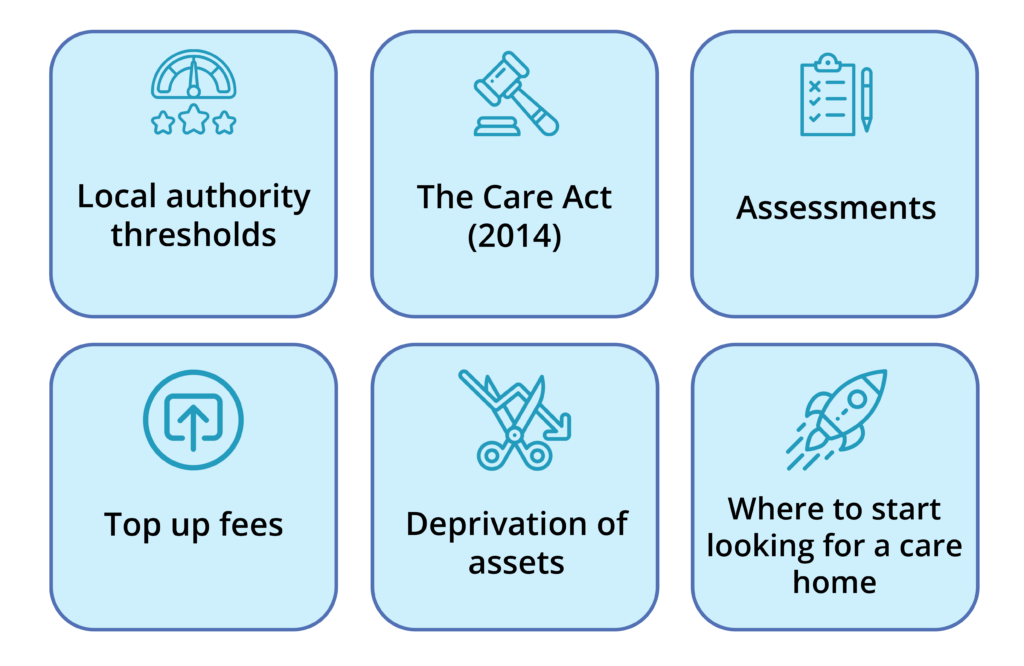

Local authority thresholds for care home fees

Each country in the UK sets a limit for how much money you can have in income, savings, property or other capital before you start paying towards your care home fees; the more money you have, the more you’ll contribute.

This means:

- If you have less than a certain amount (lower limit), your care will be fully funded by the council, also known as state-funded.

- If you have over a certain amount (higher limit), you’ll pay the total cost of your care, known as self-funded.

- If your income is somewhere in between, you’ll contribute towards your care costs with partial funding from the council.

What are the capital limits?

| England | Scotland | Wales | Northern Ireland | |

| Higher limit | £23,250 | £35,000 | £50,000 | In Northern Ireland, funding is provided by Health and Social Care Trusts rather than councils. |

| £23,250 | ||||

| Lower limit | £14,250 | £21,500 | £14,250 |

What is the care home fees cap 2025?

The Conservative government had promised to bring in a care home fees cap in England in October 2025. This would have meant no one would have to pay more than £86,000 in England for their personal care.

However in July 2024, the government became controlled by the Labour Party and Chancellor Rachel Reeves announced the care cap was being scrapped to help tackle a spending ‘black hole’ inherited from the Conservative government.

The Care Act (2014): The council’s responsibility for social care

The Care Act was introduced in 2015 to help give people greater autonomy over their care; this includes more informed decision making, a better appeals system and the option to seek independent financial advice.

The Act promoted a more personalised approach to care, moving away from a one-size-fits-all service and highlighting the responsibility of local authorities to ensure that they meet people’s individual needs.

Under this Act, local authorities have a legal duty to meet the ‘eligible’ needs of adults who live in the local area – these are the needs determined through the Needs Assessment (explored in more detail below) – when any of the following five situations apply:

- The type of care and support they need is provided free of charge.

- The person cannot afford to pay the full cost of their care and support.

- The person asks the local authority to meet their needs.

- The person does not have mental capacity, and has no one else to arrange care for them.

- When the cap on care costs comes into force in 2025, their total care and support costs have exceeded the cap.

What are the council’s duties if it is responsible for your care?

- Help you to make decisions about how you want your care needs to be met.

- Create a care and support plan to meet your needs.

- Work alongside you to ensure that care provision is positively impacting your life.

The Care Act applies to England, but there is similar legislation in place across the UK.

- Scotland – Regulation of Care (Scotland) Act 2001

- Wales – Social Services and Well-being (Wales) Act 2014

- Northern Ireland – Health and Social Care Act (Northern Ireland) 2022

Each law works to ensure that social care is accessible and inclusive.

Assessments

For your local authority or trust to determine how much, if at all, you’ll need to pay towards the cost of your care home fees, you’ll need to undergo two different assessments; a care needs assessment and a financial assessment. They are both free of charge.

Needs assessment

A needs assessment will look at how you’re managing daily life to work out what kind of support you would benefit from (what your needs are). This will address your physical needs as well as your social and emotional needs.

What information will a needs assessment look at?

- Your needs and how they impact on your wellbeing – for instance, a need for help with getting dressed or support to get to work.

- The outcomes that matter to you – for example, whether you are lonely and would like to socialise more.

- Other circumstances – for example, whether you live alone or whether someone supports you.

A professional person, such as a nurse or social worker will carry out your needs assessment, this could be over the phone or in person. They will ask you questions about what parts of daily life you’re struggling with and what you’re doing ok with.

If you have a long-term care need, you might be eligible for NHS Continuing Healthcare, which is provided through the NHS rather than local authorities. A needs assessment will be carried out to determine if you’re eligible.

If you’re not eligible, you can ask for the information gathered in the assessment to be passed on to your local council to help you obtain the care you need without having to repeat the assessment.

Financial assessment

A financial assessment, also known as a means test, will work out how much you’ll need to contribute to your care fees, if anything. This should be carried out following your needs assessment.

The assessment will look at:

- Income

- Pensions

- Savings

- Property

Property may not be taken into account in certain situations, such as if your partner or child will continue to live there when you move into a care home, but this will depend on individual circumstances.

Read more in our article here.

Top up fees

If you’re eligible for local authority funding, there will be a maximum amount that will be allocated to covering the cost of a care home that suits your needs.

If there is a particular care home you’d like to live in but your allocated funding doesn’t cover the costs, a family member or close friend may be able to pay an additional amount to cover the difference. This is known as a ‘top up fee’.

You can’t usually pay the top up fee yourself as your funding budget has already been determined through the financial assessment. However, there are certain circumstances when this might be possible. Read our article to find out more about top up fees.

Deprivation of assets

Deprivation of assets refers to when you purposely reduce the amount of capital you have in order to qualify for funding from your local authority.

As part of your financial assessment, information such as your bank accounts and how you’ve handled your money over recent months, or even years, will be assessed. If it looks as though you’ve deliberately offset some of your capital, by gifting money or making expensive purchases for example, it may be considered to be a deprivation of assets.

What about the 7 year rule?

Despite popular opinion, there is no time frame when it comes to deprivation of assets, and the seven year rule is a myth. No matter how long ago you released capital, the intention of your actions will be what matters. For example, if there was no way for you to know at the time of the action that you would need care, then any financial offsets will likely not be deemed as intentionally depriving yourself of capital. But if your care needs were increasing at the time, this may be seen differently.

Where to start looking for a care home

Once you’ve established what funding you’re eligible for, it’s time to start looking for a care home. Depending on your situation, your local authority may recommend the home(s) which is suitable for you and within your budget, but you should also have a say in this.

Search for a care home on carehome.co.uk

Whether you’re looking at self-funding or would like to check out the options that have been suggested to you, carehome.co.uk provides information about care homes located across the UK, including what facilities and services they offer as well as genuine reviews. They also list inspection ratings and detailed and transparent fee information and host a free expert care helpline to assist older people in their search for a care home.

To search for care homes in your area, visit carehome.co.uk or simply enter your location below…

Find your ideal care home

- Explore a wide range of care options and facilities

- Read independent ratings and reviews

- Connect directly with care homes to book a tour and discuss your needs